Finding calm amidst a money storm

feeling empowered to take big adventurous trips, invest in property and grab that uber home occasionally

The problem: Life in a money storm is tough

Money pouring in and out of a whirlwind of salary, food bills, meals out, rent, lunches, books, clothes, gifts, the list goes on. An unmeasured money storm that makes me nervous and panicked when I think about it. My reaction is to hold back on all spending ever, assume the worst, and horde my bucks.

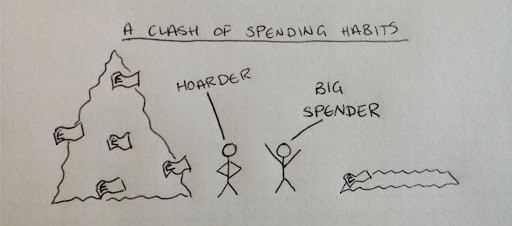

This worked fairly well as a single unit. I would accidentally save lots and live very frugally with zero treats, and then blow it all on a trip to South America, or a laptop.

When our unit grew to two people, things had to change. Ruskin isn't afraid to spend money, he likes to do the maths and spend right to the last penny. He would plan ski trips, a Thailand holiday, or even buy a snowboard. But when we hadn't quantified our typical month's money storm, this kind of spending only added to my anxiety. I was sure we were overspending.

I couldn't get on board with Ruskin’s back of the envelope estimates, and Ruskin couldn’t just blindly save like me, so we had to find something we could both buy in to.

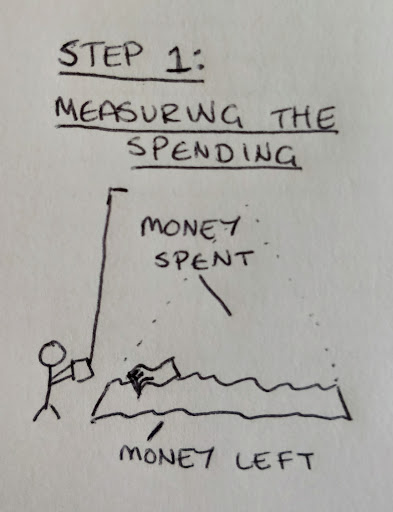

First steps: Measuring stuff

Initially we started looking back at past spends and inputting everything into an Excel file. This was when we started trying to measure how much was a normal month of spending? What could we expect to have leftover next month?

It was a bit clunky, downloading bank csvs, uploading into our own files, using different categories, and sometimes leaving long periods between check ins.

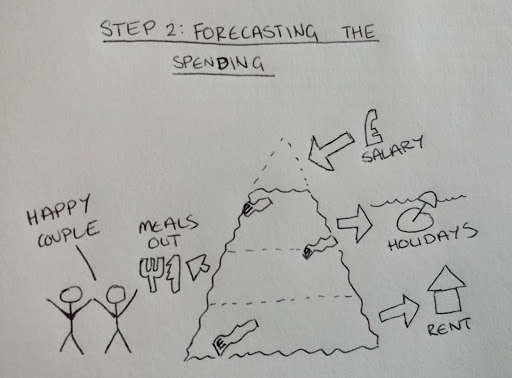

Next steps: Future forecasts

Then we discovered YNAB which ticked a lot of boxes and got us thinking about future planning, allocating all income to somewhere each month, on the fly check ins, synced across multiple devices, and also great reporting. This meant we started pulling insights from our past behaviour to forecast spending for the future.

It's fine to allocate some income to typical spends each month like supermarket, rent, lunch. But it's empowering to allocate money to important buckets for the future, like weddings, Christmas, holidays, and even bigger investments.

So for example:

- it's fine to budget £200 for the supermarket each month and monitor if you're a bit over or below the plan

- it's empowering to allocate £20 to taxis each month, and then take an Uber home from a party and not feel any guilt or budget concern

- and it’s EXCITING to put £150 towards weekends away each month, and have £450 in your pot afterwards 3 months, especially for a natural anxious hoarder like me.

Riding out the storm

This kind of budgeting has empowered us to take big adventurous trips, invest in property and grab that uber home occasionally.

I find it gives a true picture of what savings or spare cash you really have - not just what's in your bank account today, but what’s in there after upcoming commitments and life costs.

One extra perk is the few years of spending data we’ve built up, which can be important for designing lifestyle changes, such as what salary would we need if we move, or how much cash do we need to take some time off.

What do you think? How do you tame your money storm? Please feel free to leave a comment.